The Hidden Cost of Accounting Turnover in Growth-Stage Companies

by Mike Almero

3/9/20267 min read

The Question That Changed Everything

The conference room falls silent. You're three weeks into due diligence for your Series B, and the lead partner from the VC firm leans forward with what seems like a straightforward question: "Can you walk me through why your LTV:CAC ratio dropped 23% in Q3 last year?"

Your mind races. Q3. That was when Sarah ran finance—before she left for that Series C startup. You glance at your current controller, who's been with you for only two months. He's already pulling up spreadsheets, but you both know the truth: the "why" isn't in any dashboard.

The data exists somewhere. The revenue is there. The marketing spend is documented. But the context—the methodology changes, the cohort definitions, the one-time adjustments—that lived entirely in Sarah's head. And Sarah is gone.

"We'll need to get back to you on the specifics," you hear yourself saying. The investor's expression doesn't change, but you've seen that look before. It's not anger. It's doubt.

The Hidden Erosion

This scenario isn't hypothetical. It happens constantly in growth-stage companies between pre-seed and Series B. Accounting turnover doesn't announce itself with alarm bells. It erodes reporting confidence silently, one departed employee at a time, until a critical moment—like investor due diligence—exposes the fragility beneath seemingly solid numbers.

The cost isn't just a delayed funding round. It's the investor's recalculation of risk, the downward pressure on valuation, and the fundamental question now lodged in their mind: If they can't explain their past, how can I trust their projections?

Understanding how these mechanisms operate—and their cumulative impact on investor perception—is essential for building durable financial operations.

How Accounting Turnover Silently Erodes Reporting Confidence

Reporting confidence isn't a nice-to-have metric. It's your organization's ability to consistently produce accurate, timely financial information regardless of who's on the team. When accounting turnover strikes, it doesn't just create a hiring headache—it systematically dismantles the infrastructure that investors scrutinize during due diligence.

Here's how the erosion happens, mechanism by mechanism.

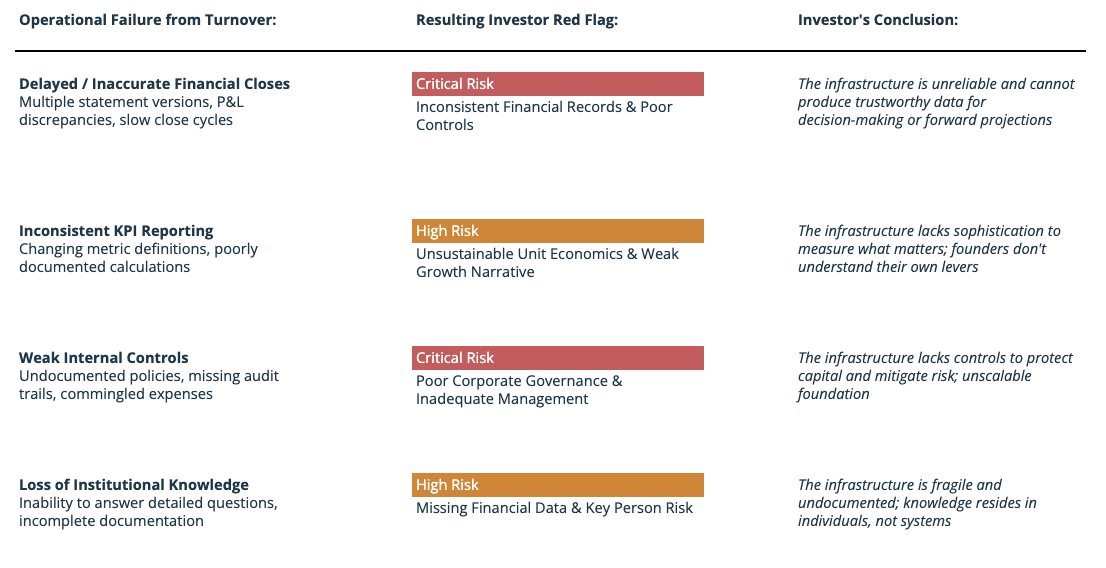

1. Institutional Knowledge Loss: When Processes Become a Black Box

Your senior accountant who just left didn't just know how to close the books. She knew why certain revenue gets deferred in Q3, how to handle that edge-case accrual for the enterprise contract, and which vendor invoices always arrive late. That tacit knowledge—the undocumented procedural nuances and historical context—walks out the door with every departure.

The result? Inconsistent execution. Your new hire reconciles accounts differently than the last person. Journal entries vary from month to month. What was once a predictable process becomes a guessing game. This isn't about competence—it's about context that was never captured in a system.

2. KPI Inconsistencies: When Your Metrics Stop Making Sense

Investors and leadership rely on KPIs to gauge company health. But nuanced metrics like CAC, LTV, and MRR can be interpreted and calculated differently depending on who's running the reports.

Without continuity, your new finance team member might calculate Customer Acquisition Cost differently than their predecessor, making period-over-period comparisons meaningless.

When your board deck shows MRR growth that doesn't reconcile with last quarter's methodology, trust erodes. Fast.

3. Delayed Month-End Closes: When Timeliness Becomes Your Enemy

Turnover creates bottlenecks. Overloaded remaining staff, inexperienced new hires struggling with the learning curve, and missing documentation all conspire to push your month-end close timeline further out. Tasks like account reconciliation and journal entry review simply take longer.

The cost? Leadership makes strategic decisions based on stale data. By the time you close the books, the insights are already outdated. And when closes consistently miss deadlines, it signals to investors that your financial operations aren't scalable.

4. Weakened Internal Controls: When Risk Exposure Multiplies

Internal controls aren't bureaucratic overhead—they're the policies and procedures that safeguard your assets and ensure reporting integrity. Accounting turnover directly undermines this framework. Key personnel departures create control gaps where one individual suddenly controls multiple parts of a transaction, increasing fraud risk. Research confirms a direct relationship between executive turnover and internal control weaknesses.

Worse, overburdened teams skip control steps—approvals, reconciliations, documentation—to meet deadlines. What looks like efficiency is actually accumulating risk that surfaces during audits or due diligence.

Strategic Insight: For growth-stage companies, scalable internal controls aren't a compliance hurdle—they're a foundational requirement for sustainable growth. Turnover exposes when controls depend on specific individuals rather than embedded systems and culture.

The Investor Lens: When Turnover Becomes a Deal-Breaker

When investors conduct financial due diligence on growth-stage companies, they're not just validating numbers—they're stress-testing your financial infrastructure. The shift from Seed to Series A/B marks a fundamental change in expectations: from demonstrating potential to proving repeatability and operational control. Investors scrutinize four critical dimensions: reporting quality and consistency, month-end close timeliness, internal control maturity, and KPI calculation integrity.

Accounting turnover directly undermines each of these dimensions, triggering red flags that can derail funding conversations entirely. Here's how operational failures translate into investor concerns:

Reporting Confidence: The Foundation Investors Assess

Ultimately, investors use due diligence to evaluate whether your financial infrastructure can responsibly deploy and manage institutional capital. High accounting turnover signals immaturity—not just in your finance function, but in your entire operational discipline.

Reporting confidence—your organization's ability to consistently produce accurate, timely financial information regardless of personnel changes—becomes the defining metric of investor readiness.

When investors encounter delayed closes, inconsistent KPIs, and control gaps, they conclude the company is not audit-ready and financial operations are not scalable. This forces difficult choices: pass on the deal, demand lower valuation to compensate for operational risk, or impose restrictive covenants. The instability signaled by accounting turnover directly impacts deal outcomes—and not in your favor.

The solution isn't hiring your way out of the problem—it's building systems that outlast individuals. Here's how growth-stage operators structure financial operations to withstand turnover and signal maturity to investors.

Building Turnover-Resistant Financial Operations

The path to reporting confidence isn't hiring better accountants—it's building better systems. Growth-stage companies that withstand turnover share a common trait: they've shifted from relying on individual expertise to engineering resilient infrastructure.

Here's the four-pillar framework that transforms fragile financial operations into investor-ready infrastructure:

1. Documentation and Playbooks: Institutionalize Knowledge

Your accounting processes shouldn't live in someone's head. Document them so they survive personnel changes.

Create process playbooks that capture the "why" and "how" for critical workflows like revenue recognition, month-end close, and accrual calculations. Start by interviewing your current team: "What do you do that no one else knows how to do?" Document those answers.

Build a centralized digital repository using cloud-based document management systems. Ensure secure access, version control, and clear naming conventions.

Standardize with templates and checklists. Create step-by-step SOPs for repeatable tasks, using screenshots or short videos. Keep them simple enough that a new hire could follow them on day one.

2. Intelligent Automation: Reduce Manual Dependencies

Automation isn't about replacing people—it's about making your financial operations resilient to turnover by reducing reliance on manual tasks.

Automate accounts payable and receivable workflows. Tools like Bill.com handle invoice capture, approval routing, and payment processing, eliminating manual data entry and reducing processing time.

Implement automated reconciliations and close processes. Modern platforms like NetSuite or Sage Intacct consolidate data automatically and handle complex tasks like multi-entity reporting.

Start small with high-impact areas. Identify bottlenecks first, then select scalable cloud-based tools that integrate with your existing systems.

3. Cross-Training: Distribute Expertise

A single point of failure in your accounting team is a risk you can't afford. Cross-training builds flexibility and reduces dependency on any one person.

Implement job rotation for critical functions. Have team members shadow each other's roles quarterly, starting with high-risk areas like payroll or financial reporting.

Document as you cross-train. Use training sessions as opportunities to capture institutional knowledge in your playbooks.

Build natural checks and balances. When multiple people understand a process, you create organic fraud deterrence and improve internal controls.

4. Process Standardization: Ensure Consistency

Standardized processes ensure tasks are performed uniformly, regardless of who's doing them. This is non-negotiable for investor readiness.

Create standardized close calendars and checklists. Define exactly when each task happens, who owns it, and how to verify completion. Track adherence monthly.

Establish approval workflows and access controls. Use software to enforce separation of duties and role-based permissions, reducing fraud risk and strengthening governance.

Strategic Insight: Companies that implement all four pillars typically see significant reductions in onboarding time, fewer internal support tickets, and faster due diligence cycles. The ROI isn't just operational—it's strategic positioning for your next funding round.

These aren't one-time projects. They're ongoing investments in organizational resilience. Start with the area causing the most pain, then expand systematically. The companies that scale successfully are those that build durable systems before they desperately need them.

Your Next Steps: Building Reporting Confidence

Reporting confidence isn't built overnight, but it doesn't require massive teams or expensive consulting engagements. Start with these focused interventions:

1. Audit Your Documentation Gaps

Spend two hours mapping your critical financial processes. Which ones exist only in someone's head? Start there. Document your month-end close checklist, KPI calculation formulas, and revenue recognition policies first.

2. Automate Your Highest-Risk Manual Process

Identify the one recurring task most vulnerable to human error or personnel dependency—often bank reconciliations or expense categorization. Implement automation for that single process this quarter.

3. Institute Weekly Cross-Training

Dedicate 30 minutes each week for team members to shadow critical tasks outside their primary role. Rotate responsibilities for routine close activities quarterly.

4. Create a Financial Operations Playbook

Build a living document that captures standard operating procedures, system access protocols, and escalation paths. Update it monthly as processes evolve.

5. Establish Monthly Systems Reviews

Schedule recurring 60-minute sessions to assess process performance, identify bottlenecks, and refine documentation. Treat financial infrastructure as product, not overhead.

Conclusion

Systems are your competitive moat. Growth-stage companies that build turnover-resistant financial operations raise capital faster, command higher valuations, and scale with confidence. Robust internal controls and process standardization aren't compliance burdens—they're strategic infrastructure that signals operational maturity to investors and enables sustainable growth.

The founders who win don't just hire great accountants. They build financial operations that outlast any individual contributor—systems that produce reliable data, support informed decisions, and prove investor readiness regardless of who's running them.

Table: Operational Failures and Investor Red Flags

If accounting turnover has started slowing decisions or creating uncertainty in your numbers, it may be time to rethink how the team is structured. Ledgion connects companies with pre-vetted accounting professionals who bring consistency from day one.

Explore how a more stable accounting team can look → https://ledgionfso.com/

The Right People, In The Right Seats. Remotely.

© Ledgion Global Solutions, Inc. 2026. All rights reserved.